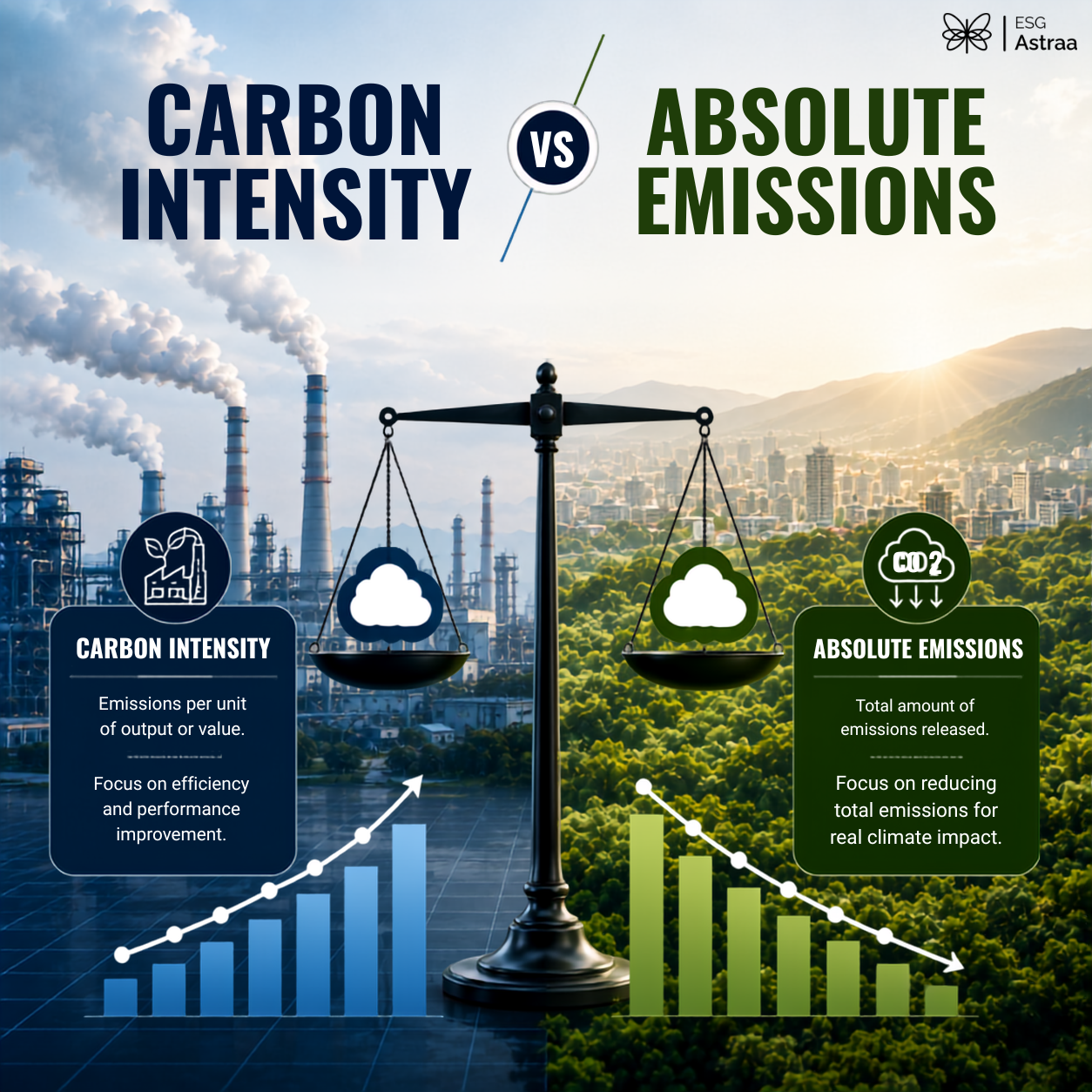

Carbon Intensity vs Absolute Emissions

Why the Metric You Choose Changes Your ESG Story Completely?

Reading Time

4 min

Article Sections

6

Share Links

3

On This Page

Article Section

Introduction

A fast-growing technology company last year highlighted a steady decline in its emissions intensity per unit of revenue, even as its global CO2 emissions by year rose in absolute terms because the business itself had grown faster than its efficiency gains.

This is not a reporting error; it is a choice. Companies reporting scope 1 2 3 emissions can present the same underlying data as either an intensity ratio or an absolute figure, and each version supports a different narrative about progress.

The metric a company leads with says as much about its ESG story as the number itself, and investors are increasingly asking to see both side by side rather than accepting whichever one looks better.

Article Section

How Intensity and Absolute Metrics Are Actually Calculated?

Scope 1 2 3 emissions cover direct operational emissions, purchased energy, and value chain emissions respectively, and scope 1 and 2 emissions form the base most companies report on first because they sit within direct operational control.

ISO 14064 and ISO 14064-2 set out how organizations should quantify and report greenhouse gas emissions, but neither standard mandates whether a company should lead with an intensity ratio or an absolute figure, leaving that choice open to interpretation.

Global GHG emissions by sector and global CO2 emissions by sector data show that some industries, such as manufacturing, are naturally suited to intensity reporting given output variability, while others with stable production volumes are better judged on absolute trends alone.

Article Section

What Each Metric Reveals and What It Hides?

Why Intensity Metrics Flatter Growing Companies?

A company reporting scope 1 and 2 emissions intensity can show consistent year-on-year improvement simply by growing revenue faster than emissions, even when ghg emissions scope 1 2 3 in absolute terms are rising, because the ratio divides emissions by a denominator that is also increasing.

How Absolute Emissions Tell a Different Story?

Global CO2 emissions by year data, when applied at the company level, strip out the denominator effect entirely and show whether a company's total climate footprint is actually shrinking, which is often a less flattering picture than the intensity figure suggests, particularly against global greenhouse gas emissions by sector benchmarks.

The Net Zero Ambiguity Problem

Net zero emissions by 2050 commitments are frequently built on intensity-based interim targets, meaning a company can appear on track toward net zero carbon emissions while its actual carbon net zero date, measured in absolute terms, keeps slipping further out.

What Reporting Standards Actually Require?

ISO 14064 and its companion standard ISO 14064-2 require accurate quantification and verification of emissions data, but they leave the choice of presentation, intensity or absolute, to the reporting company, which is precisely where most of the ambiguity in ESG storytelling originates.

Article Section

Getting the Disclosure Right

Choosing the Right Metric for Your ESG Story

Companies should report scope 1 2 3 emissions alongside relevant GHG emissions by country or sector benchmarks in both intensity and absolute form, rather than choosing the version that reads best in a single reporting cycle.

Avoiding Carbon Neutrality Claims That Don't Hold Up

Carbon neutrality claims that rely solely on intensity improvements or offset purchases invite scrutiny once compared against a company's carbon neutral 2050 roadmap and its actual absolute emissions trajectory, so disclosure should show the underlying assumptions rather than the headline claim alone.

Preparing for Scrutiny on Both Metrics

As net zero greenhouse gas emissions commitments mature, companies should expect investors to request both figures together, using global GHG emissions by sector data as a reference point, making dual disclosure a defensive necessity rather than an optional extra.

Article Section

Conclusion

The underlying data rarely changes between the two metrics; what changes is which trend a company chooses to foreground, and that choice increasingly reads as a signal in itself.

Companies that disclose both intensity and absolute figures transparently, rather than defaulting to whichever looks better, will be better positioned as investors get more comfortable reading both lines on the same chart.

Article Section

Frequently Asked Questions

What is the difference between scope 1, 2, and 3 emissions?

Scope 1 covers direct emissions from owned operations, scope 2 covers purchased energy, and scope 3 covers value chain emissions outside a company's direct control.

What is carbon intensity versus absolute emissions?

Carbon intensity measures emissions relative to an output such as revenue or production volume, while absolute emissions measure the total volume of emissions regardless of business size.

What does ISO 14064 require for emissions reporting?

ISO 14064 sets requirements for quantifying, monitoring, and verifying greenhouse gas emissions, but does not mandate whether a company reports intensity or absolute figures.

What does net zero emissions by 2050 actually measure?

It typically refers to a company's commitment to reduce or offset emissions to net zero by that date, though the interim targets used to track progress can be based on intensity or absolute figures.

Can a company claim carbon neutrality without cutting absolute emissions?

Yes, if the claim relies on intensity improvements or purchased offsets rather than a reduction in the company's total absolute emissions.

Keep Reading

Related Blogs

All Industries

ESG and the Indian SME

Why Small Suppliers Are Suddenly Under Pressure From Their Largest Clients

Read more

All Industries

Five ESG Metrics Every Investor Pitch in India Should Now Include

Most Still Don't Know

Read more

All Industries

Carbon Credits vs Carbon Offsets

Understanding the Difference Before Making Climate Claims

Read moreNext Step

Ready to turn ESG complexity into strategic advantage?

Talk to ESG Astraa about disclosures, climate strategy, governance controls, and execution support for your team.